Advertisement

Did Employer Penalties Work In Massachusetts?

WBUR

Think back, way back, to the last days of winter, 2006: it looked like negotiations around a landmark health care law in Massachusetts might fall apart.

The sticking point was whether to include a health insurance mandate for employers and if not, how to make sure they helped cover the uninsured. The deal that broke the logjam was largely symbolic, although lawmakers didn't say that at the time. Now, it's clear to many that the penalties have had little effect on achieving near universal coverage.

First, a quick refresher:

The state’s health coverage law included two largely symbolic penalties for employers who didn’t get with the program by providing adequate employee health insurance.

1) The Free Rider Penalty

It's supposed to catch employers whose workers use more than $50,000 worth of "free care" in one year. (These are costs covered by what used to be called the "free care pool," and what is now the "health safety net." Essentially, it's patient care that hospitals don't expect to be paid for, so they bill the state.) For instance, if an uninsured worker who has a serious accident or illness, gets care in a hospital, and doesn’t pay the bill, the law says the state can fine that worker’s employer between 20% and 80% of the care. A report out last week says no one has paid the fine since the law took effect. Initial estimates suggested it might raise $50 million. In the final bill, this penalty was waived for employers who let workers buy health insurance on a pre-tax basis. No one expected the Free Rider penalty to raise much money and it hasn’t: $0 to be clear.

2) The Fair Share Rule

It says that employers must offer “fair and reasonable” coverage or pay a fine of $295 a year for each employee.

The rule only applies to businesses with 11 or more workers. The penalty has not increased since the law was passed in 2006. To date, the penalty has raised $57 million, including $20 million this year, according to the latest state figures. It was expected to raise about $45 million a year.

The money helps fund subsidized coverage (a.k.a Commonwealth Care) for low and moderate income residents.

Some consumer advocates argued early on that the employer penalties were too lax (and some say they still are). But there’s a strong argument that employers are doing their part to support near universal coverage and it has little to do with the penalties.

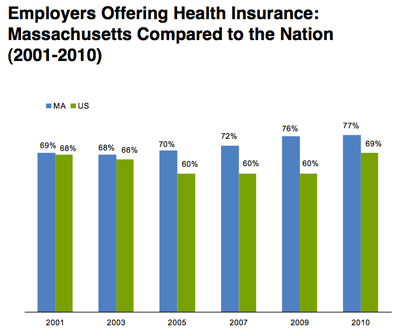

The argument centers around this fact: employer coverage in Massachusetts has increased every year since the law passed. Employer coverage nationally, on average, dropped steadily during the same period, but started to climb again in 2010. Last year 77% of firms in the Bay state offered health insurance compared to 69% nationally, the state reports.

Employer coverage increased in Massachusetts even though health insurance premiums rose in the range of 10% every year. So worries that employers would drop coverage and pay the much cheaper penalty ($295 a year) instead, were largely unfounded, says Rick Lord, president and CEO at Associated Industries of Massachusetts.

Why are employers in the Commonwealth continuing to offer health insurance even though it’s becoming a bigger strain on their budgets? Business leaders say it has little, if anything to do with the threat of fines.

“Employer penalties have played a very minor role in Massachusetts health reform,” says Michael Widmer, president of the Massachusetts Taxpayers Foundation. “They were more of an appendage to the law, but they were symbolically important and part of a political compromise” that helped the law clear a final hurdle before passage.

Widmer and others agree there are three reasons why more employers are offering health insurance:

-- To hire qualified employees, employers must provide good benefits.

-- Employees demand health insurance in particular to avoid the individual mandate penalty.

-- Massachusetts has traditionally had high rates employer coverage.

In short, many employers say there’s a culture of providing good insurance in the Commonwealth.

It’s hard to say how the lessons from employer penalties in Massachusetts will resonate as stiffer penalties in the Affordable Care Act take effect.

“A key lesson from Massachusetts is that reform must be built on the circumstance and character of a given state” and the employer community in that state, says Widmer.

Consumer advocates agree that employers are doing their part to offer insurance, but many say the unresolved question is: Can people afford coverage. They point out that the number of workers who are taking employer-sponsored health insurance in Massachusetts is down.

“There is more and more cost shifting to consumers, with high co-pays and co-insurance,” says Celia Wcislo with SEIU 1999, a union that represents many health care service workers. “The cost shifting means there are more and more disparities in how much care people receive. It’s financial rationing of care.”

Can we continue to afford near universal health coverage? That’s the next lesson for Massachusetts.

This program aired on August 12, 2011. The audio for this program is not available.