Advertisement

A Behind-The-Ledger Look At Partners HealthCare's Billions

Partners HealthCare, the state's biggest and richest hospital system, fills me with confusion and cognitive dissonance.

Partners does angels' work: all the cutting-edge research and top-flight tech at Mass. General, Brigham and Women's and other hospitals. But when it comes to health care costs, Partners is seen as one of the prime culprits behind the high prices that are driving up our health insurance premiums and bedeviling our economy.

(An editor-friend prompted, "So it seems to you that Partners epitomizes almost everything that's right and everything that's wrong with the American health care system?" "Damn, you're good," I said.)

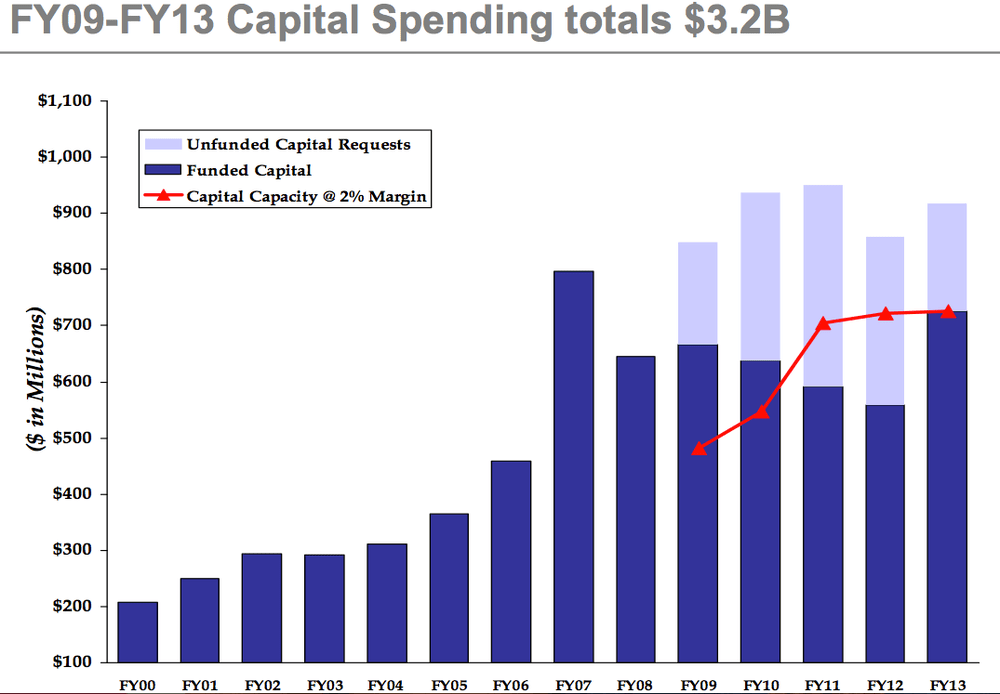

I went to see Peter Markell, chief financial officer of Partners HealthCare, about a fascinating set of Partners financial slides that were until recently knocking around the Internet. Peter provided updates on the data, and explanations. The first slide, above, shows the Partners system's capital spending total for 2009-2013: a staggering $3.2 billion. That's a scale that virtually none of the state's other hospitals can even dream about.

[module align="right" width="half" type="pull-quote"]'People want to walk into a place that makes them feel good.' ('Good, yes,' I thought. 'But $687-million-good?')[/module]

Peter described a dynamic process in which Partners holds its operating margin — its excess of revenue over expenses — at roughly 2%, then chooses the best from among a superabundance of staffers' ideas for spending its capital budget.

That sounds like the best of choices, but others question whether the hospital system is making the right choice writ large, by spending so hugely. Professor Nancy Kane of the Harvard School of Public Health says she sees these Partners' slides' message as "Whatever we want to spend, we should be able to spend, regardless of the cost or affordability to taxpayers and Massachusetts small business premium payers."

The big picture

I have to say, when Partners officials defend their high prices by citing their 24-hour burn unit or their money-losing psychiatric care, I'm left unsatisfied. Thank goodness they offer those services, but those expenses account for only a tiny portion of an $8-billion annual budget. (Mental health and substance abuse services cost Partners $60 million last year, the latest annual report says.) There are other good reasons for high Partners prices. Among them: Their top hospitals care for some of the sickest patients.

But I'm trying to look at the big picture. That's what Partners CEO Dr. Gary Gottlieb said to do when he testified at a state hearing in June. We should not, he said, focus on high Partners prices for individual services (like Rachel's sky-high ultrasound price tag, for example.) We should look at the "range of services" that a hospital system offers, including its money-losing ones, and at how hospitals organize their finances.

[module align="right" width="half" type="pull-quote"]'Did it ever occur to them that if you have to make 40% in margins off of small and large employers in order to cover the cost of your government business, that maybe they should trim their capital and investment plans a tad?'[/module]

The 2% margin that Partners maintains sounds modest. But $3.2 billion for capital spending does not sound modest by any stretch, even for a nine-hospital system. And going forward, capital spending tends to bring gifts that keep on taking.

If you build a building — like Massachusetts General Hospital's new Lunder Building, whose total cost is estimated in the Partners annual report at $687 million — you have to keep maintaining it and staffing it and heating it. Partners has launched a cost-cutting initiative called "A Case for Change," but these four years averaging $800 million in investment a year don't bode well for major cost-cutting in the future.

Partners capital spending goes far beyond new buildings. It also includes renovations of existing buildings and computer systems. Here's a breakdown of where their capital spending money goes, with thanks to Partners spokesman Rich Copp:

-New facilities: 20%

-Information Technology — 25%

-Facility maintenance and upkeep — 40%

-Research — 10%

-Other — 5%

"We're not perfect," Peter Markell said. "Do we make every decision right? No. But we try to run a very balanced system. Somebody could challenge our individual choices, but they're all investment choices. If the modern-day thinking is that quadruple rooms and double rooms don't really work because of gender, and infectious disease, then the new facilities you build are going to have more private rooms. There's a little bit of cost to that."

Also, looking ahead, he said, "People want reasonably first-class facilities. People want to walk into a place that makes them feel good."

("Good, yes," I thought. "But $687-million-good?")

I think maybe Peter saw my reservations on my face. Yes, he said, "sometimes bricks and mortar can be overblown, and it's a challenge to balance that." Investing in the latest diagnostic equipment is important as well, he said: "If you think about medicine going forward, the real art is who can isolate the issue quicker than someone else, because a lot of money is spent just trying to figure out what the problem is."

Overall, he said, Partners has compared its cost structure with other academic medical centers that it considers reasonable competitors across the country, and it comes out basically "in the middle of the pack."

Statewide, of course, where the great majority of its competitors are, it's a different picture. The capital spending at Partners dwarfs virtually anyone else's. One hospital expert estimated that per patient, it could be several times the average.

Attorney General Martha Coakley has repeatedly pointed to Partners costs as a driver of the state's ever-higher insurance premiums. The reasoning: The higher payments that Partners receives allow it to invest in facilities and staff in ways its competitors can't. That lets it build its brand and market share, which gives it leverage with insurance companies, which lets it charge them higher prices, which they pass on to consumers — and on and on.

Which brings us to the next slide:

This slide shows what many of us already know: Private employers — and we workers — are compensating for serious underpayment by the government programs Medicaid and Medicare, which provide coverage for the poor and elderly.

"If the government sector paid cost," Peter said, "the prices we charge the private sector would be 20 to 22% less." The government shortfall has been increasing, he said, "and the private payer marketplace is saying 'No more.' How it will work out remains to be seen."

Of course, there's also another way to look at this slide. Commented one health care analyst who'd like to remain anonymous:

"Peter Markell is extensively quoted as saying that they aim for 2-3% overall margins. He never mentions that he aims for a 40% margin from MA private employers! Did it ever occur to them that if you have to make 40% in margins off of small and large employers in order to cover the cost of your government business, that maybe they should trim their capital and investment plans a tad? The businesses who are paying for these monuments didn't get a say in the capital planning process. I would venture to say most of those businesses approach their own capital needs with more restraint."

"You can deconstruct the Partners mantra that they simply target a 2% margin. Sounds reasonable right? In fact kind of a bargain. But the problem is that with their market dominance, they have the luxury of having commercial insurers 1) fully cross-subsidize their Medicaid and Medicare losses and 2) cover any level of capital spending they think is appropriate. With the combination of these two things they can decide what a 2% margin looks like. They could just as easily have had a 2% margin with half that amount of capital spending and kept their rates much more affordable. They will point to national capital investment benchmarks, but this ignores the imbalance in the Boston market."

Money makers and money losers

And now, one last set of slides: In the big picture, there are striking financial winners and losers among the medical specialties. Peter explained that these income gaps are largely the artifacts of history, based on traditional Medicare rates.

First, isn't it just downright interesting to see that cancer is a big money-maker and obstetrics is a money sink? I hear that this sort of breakdown is similar at other hospitals, not unique to Partners. It's just rare to see it laid out so clearly. And it's frankly a little shocking to see how heavily cancer care bears the burden for the rest of us. Below, you'll see that imaging — MRIs and other scans — is also quite the moneymaker for Partners — as Rachel's ultrasound post suggested.

So what are we to make of all this? My cognitive dissonance continues. We could rejoice that we have medical institutions afloat in money. We could mourn that much of that money comes from our premiums, and we have no say on how it's spent.

Two hospital experts I consulted said that Partners should not be criticized for its corporate business plan — it plays by the rules. "What we have to criticize here," one said, "is the fact that the state and the insurance companies let them get away with this tax on health care."

Readers, members of CommonHealth's prodigious brain trust, I'd like to ask you. What are your takeaways from these slides? And what are the implications for Massachusetts health care reform, going forward?

One final note on going forward: Peter and others predict that health care capital spending will get tighter, but The Boston Business Journal reported here in January that:

Partners Healthcare , the state's largest network of hospitals and physicians practices, disclosed in a recent bond-offering statement that it intends to spend approximately $3.1 billion on construction and other capital upgrades over the next five years.

The disclosure was made Jan. 13 amid a flurry of filings for Partners bond offerings set to mature through 2046.