Support WBUR

The Education Bubble, Part 1: Sky-High Debt Is 'Overwhelming' Burden

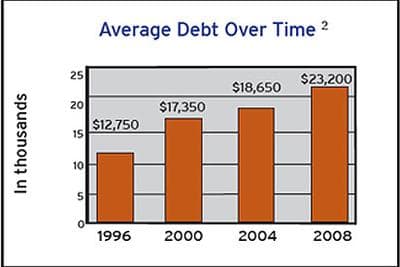

As college tuition costs keep rising, student loan debt has increased significantly. Two-thirds of students take on loans, with the average debt load now more than $23,000. And as there’s a renewed push for youths to attend some college, there’s also worry that debt levels and default rates will continue to rise as well. Part 1 of a WBUR Series: The Education Bubble.

BEVERLY, Mass. — The chapel at Endicott College rings out cheery tunes like "Rainbow Connection" from "The Muppet Movie." It’s an idyllic campus with sloping green lawns and man-made lakes with fountains. On a bench by a lake, graduate Nicole Benson sits, taking it all in.

“I honestly don’t really remember why I decided to come here," Benson says. "I think location had a lot to do with it. My mother loved it. It’s a small and quiet campus."

Benson graduated in 2007 and had major sticker shock: She found out she owed $90,000.

“And it was very, very devastating,” Benson says. “It was very shocking. I mean, just to look at a number like that at 22 years old is very overwhelming.”

She had taken out only $45,000 over the course of her four years of study. One of her eight loans is a federal loan but the rest are from private banks with interest rates as high as 15 percent. The interest on the private loans began accruing as soon as she got them.

Endicott is a small college which, when she attended, cost $31,000 a year. It doesn’t have a large endowment, so most students face a $7,000 gap in their financial aid packages. That means that after federal loans, grants and scholarships, students and families who don’t have the means turn to the private market to pay.

“My mother kind of pushed me to go to school," Benson says. "I just never had anybody say to me, 'Wait a minute, this is going to be expensive.' I honestly just had absolutely no idea.”

Benson’s mother handled most of the federal and private loan paperwork; Nicole just signed. Benson’s parents didn’t go to college and didn’t understand the loan process. Her mother and her grandmother co-signed some of the loans and are also behind on payments.

They were all making the same calculation: It would pay off because she would get a job and be able to afford and pay off the loans.

Endicott told her that with her degree in hospitality management she could make $50,000 a year. And she did get a job after she graduated, but was laid off in 2009 when the economy went south.

“I’ve cried a lot,” Benson says. “It’s been very, very emotional. It’s definitely, it’s taken its toll on a lot of aspects of my life. I’m very stressed out, very overwhelmed and very unsure of what I should do."

"I worked so hard and I really have nothing to show for it, you know. I live in the cheapest place available to me. I drive a car that is barely running."-- Nicole Benson

The harassment came in the form of phone calls — sometimes 20 to 30 a day — from her creditors.

“I tried to, I would beg them," Benson says, "I’d say, 'Look, I don’t have a job, I don’t know what you want me to do.' "

Now Benson has a bookkeeping job that pays by the hour. But her loans have grown to nearly $98,000 and her loan payments are more than $1,000 a month. She says to make a dent in what she owes, Benson figures she would have to pay $3,000 a month.

“It’s (an) unrealistic expectation of the payments that I should be able to make," Benson says. "I’m like, 'With what money?' " She chokes back tears.

Even though college graduates earn nearly two times more than those who just get a high school diploma, in her case that’s little consolation. She’s thought about bankruptcy, but it wouldn’t help because federal and private student loans cannot be dismissed in bankruptcy. She’s stuck with this debt for decades to come.

“I don’t know if I’ll ever be able to get a mortgage and buy a house," Benson says. "It’s looking pretty doubtful right now.

“It’s very disappointing that, like, I worked so hard and I really have nothing to show for it, you know. I live in the cheapest place available to me. I drive a car that is barely running. I have absolutely nothing to show for absolutely busting my ass all the time."

Student Loan Resources:

Recently, Benson, working with a pro-bono lawyer, was able to reach an agreement with two of the companies holding her loans to lower her payments. But the other private banks won’t accept a deal. So she’s about to join a growing trend and default on some of her debt. The U.S. Department of Education expects almost 7 percent of students to default on their loans for fiscal year 2007 — the highest rate since 1998.

To the people who say, "It’s all her fault, she should have known what she was getting herself into," Benson agrees. And she makes it very clear she wants to repay her loans. But she wants others to understand the larger consequences in the hope that the private student loan system will be reformed.

“If such an enormous amount of the young adult population is in so much debt now it definitely will affect the economy for years and years to come,” she said.

A recent poll from Harvard University found that a majority of young adults is concerned about meeting their bills.

Benson doesn’t blame Endicott College for getting her into debt. The school says it tells parents to at least pay the interest on private loans and go on monthly payment plans with the school, which are interest free. But, the school says, the parents choose to stick their heads in the sand. That’s basically what Benson and her family did, and now, she’s paying the consequences.

This program aired on May 24, 2010.