Support WBUR

'Greedflation': A once fringe theory of inflation gains momentum

A pandemic, war in Ukraine, supply chain breakdowns — all led to soaring prices.

Some of those forces have eased, but prices haven't. Economist Isabella has a theory about this. She calls it 'sellers’ inflation.'

"This was considered kind of fringe idea. Because I think it in many ways doesn’t fit with the macroeconomic framework that economists tend to have on their minds," Isabella Weber, assistant professor of economics at the University of Massachusetts, Amherst, says.

But Weber says businesses are now keeping prices high, simply because they can.

"The danger is that corporations have now learned how this works, they know that if they are hiking prices their competitors are also hiking prices in this kind of situation," Weber says.

"If there was another major shock, the chances are they would be even quicker to move to that kind of playbook."

Today, On Point: 'Greedflation,' a once fringe theory of inflation gains momentum.

Guests

Isabella Weber, assistant professor of economics at the University of Massachusetts, Amherst. Author of How China Escaped Shock Therapy: The Market Reform Debate. Her recent paper is titled Sellers’ Inflation, Profits and Conflict: Why can Large Firms Hike Prices in an Emergency?

Also Featured

Justin Wolfers, professor of public policy and economics at the University of Michigan.

Transcript

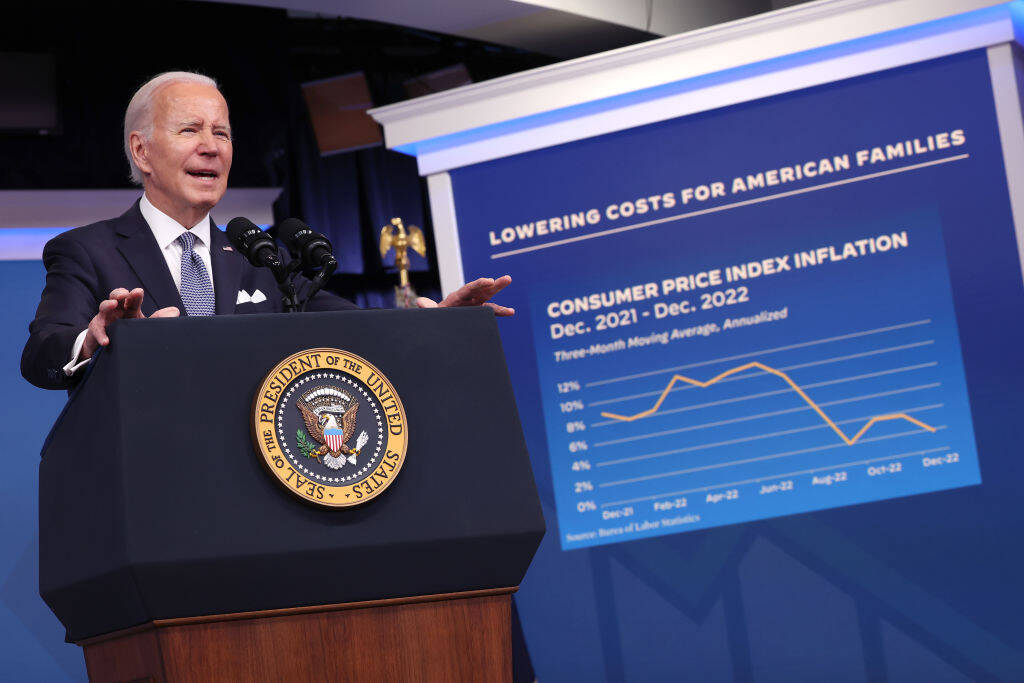

MEGHNA CHAKRABARTI: In December 2021, University of Massachusetts economist Isabella Weber looked at spiraling inflation. She saw a number of drivers for those ever-increasing prices, but there was one she thought no one was talking about. An explosion in corporate profits. In 2021, U.S. profit margins have reached levels not seen since the aftermath of the Second World War, she wrote in the British newspaper The Guardian.

So Weber made a radical suggestion, quote: "The government could target the specific prices that drive inflation. Instead of moving to austerity, which risks a recession."

Well, the response from just about every established corner of economics was unanimous. Heresy, they shouted. Liberal economist and New York Times columnist Paul Krugman went so far as to tweet, quote, "I'm not a free market zealot, but this is truly stupid."

But then something interesting happened. Prices stayed high, even though some of the inflationary drivers have eased a bit.

And then earlier this year, Albert Edwards, global strategist at the massive French bank Societe Generale, released an astonishing note saying, quote, "How wrong I was to assume that margins would have declined by the end of last year." He called, quote, "supernormal profit margins a big issue for policy makers that simply cannot be ignored any longer."

Around the same time here in the United States, Fed vice Chair Lael Brainard gave a speech at the University of Chicago, of all places, saying, quote, "Overall, the labor share of income has declined over the past two years and appears to be at or below pre-pandemic levels. While corporate profits as a share of GDP remain near postwar highs."

Brainard described it as a 'price price spiral,' where prices are still rising faster than the material costs to make those products. Even economists at the insurance company Allianz estimate that when it comes to the high cost of food, right now, about 10% of that rise is due to corporations seeking higher profits. So has Isabella Weber been vindicated? Is there something to her theory that part of what we're seeing now is due to what we in the media have taken to calling greed flirtation, though Professor Weber prefers to call it sellers' inflation. And she joins us now. Professor Weber, welcome to On Point.

ISABELLA WEBER: Thanks so much for having me back. Hi.

CHAKRABARTI: So have you gone from Pariah in the economic world to the most talked about economist and sought after economist right now? Because I'm seeing that the same central bankers and lawmakers and think tankers and academics who once were trying to laugh you out of the room, they're calling you now, is that right?

WEBER: I mean, inflation is probably one of the most complicated economic problems. So I would say the battle is now over, but it's certainly been a big turnaround.

CHAKRABARTI: But tell me more. I mean, because Axios reports that your phone is ringing off the hook. Who's calling you?

WEBER: I mean, it's been kind of a trajectory of change. Probably the most dramatic event was in last fall, actually, when the German government called me to work for them on gas price stabilization, because the gas price shock to the German economy had just become so, so, so large that households and firms could no longer pay these extremely high gas prices.

So that the government decided to step in and set up a commission to design a policy that was pretty much along the lines of what I had been arguing in the German context. So that was probably the most unexpected kind of turn around to sit there on a commission designing a policy that followed my basic principles with a budget of almost 5% of GDP at our disposal. And that was certainly quite dramatic.

CHAKRABARTI: So the principles being introducing some kind of price stabilization.

What I have been arguing is that there's one part where consumers and firms cannot save.

WEBER: Yes. So what I have been arguing is that there's one part where consumers and firms cannot save, which is basically their inelastic demand, as economists would say. And then there's another part where you can say everybody can react to price signals. I mean, if you think of it from the perspective of a consumer, you can say that you turn down the temperature in your room a little bit, that you take a shower less frequently, that you cook warm meals less frequently. But there's a limit to all of that, right?

So the idea was to protect that like essential part of consumption with a price sterilization measure while keeping the market signals up at the margins. And I won't bore you with the details of the policy that we implemented, but that was a basic, basic idea.

Now, I feel like in recent weeks there has been a new wave of all of this. I mean, it seems like the media is really catching up to this question of what is the role of profits and inflation. I mean, there has been very major reports and basically all major media outlets from The New York Times, Wall Street Journal, Financial Times and so on, and not only in English, but in several languages.

CHAKRABARTI: Okay. So what I'd like to do is a little later in the show, Professor Weber, we're going to talk about there's still considerable pushback to the theoretical framework that you offer here. So we'll do that a little bit later. But I want to just kind of go through it in a little bit of detail because you have coauthored a couple of papers specifically about why you and your coauthors see that industries can and do continue to hike prices.

Even though in the pandemic and post-pandemic period, even though they have experienced some price stabilization on their inputs. So let's use an example here, because I'd like to just make it real for folks, because in your paper you talk about, for example, PepsiCo, right? Massive global company in the food and snacks and drinks business. And you've looked at not just their earnings records, but what CEOs and CFOs say, what they literally say, during their earnings calls about the decisions they have behind their pricing.

CHAKRABARTI: So let's play we've got here a clip from a 2021 first quarter earnings call from Pepsi. So this happened in April of 2021. An analyst asks executives about Pepsi's historically high prices and if the company would be comfortable continuing with a price over volume approach, as they called it. So here's how executives answer. The second voice that we'll hear is Ramon Laguarta, Pepsi CEO. And the first you're going to hear is Hugh Johnston. He's the CFO of Pepsi, who talked about what he sees as the right way to compete.

JOHNSTON: Which is primarily around innovation and brand building and execution. So we think the environment is well set up where pricing can be positive going forward, that that's not a temporary thing based on what's happening in the environment right now.

LAGUARTA: ... We're seeing everybody becoming more capable and knowledgeable on consumer insights and applied to promotions and pricing and elasticities. And so we're going to see more application of those multiple levers, rather than just driving prices down, which I don't think is the big idea for anybody in the industry.

CHAKRABARTI: Okay. So Professor Weber, initially before that, Pepsi was saying they had to raise prices because again, they were suffering from inflation and supply chain problems like everybody else was. But by the time we get to the first quarter of 2021 here, what do you hear in that moment from the earnings call?

WEBER: Yeah. Maybe to take a little step back just to think about this as a process. So there have, of course, been major cost shocks, right? So there have been energy prices going up, food prices going up and so on. So a company like Pepsi both, of course, has faced very major cost increases.

CHAKRABARTI: You call this the impulse stage.

WEBER: That's right. Yeah. So there's an impulse that comes basically from the shutdown of the economy, which resulted in the reduction in capacity in all sorts of critical areas like energy, like raw materials, which then when the economy picked back up and demand started to increase, did not pick up at pace, which meant that in response to that, prices for things like energy started to shoot up. Which then created a cost impulse to companies that are using energy, that are using transportation services, that are using food inputs and so on.

And reacting to these cost shocks, firms basically started to raise their prices to protect their profit margins. Now, if you protect your profit margin, you actually have to increase your price more than your cost. Because if you imagine that, let's say your product costs $100 and you have a cost of $80, then you would have a profit margin of $20. Now, suppose costs go up by $5, if you now were to raise your product by just $5, you would have $105 in price. Right? Then in relative terms, your profit margin over the total price would have gone down.

CHAKRABARTI: Because it's one it's 20 over 105 now.

WEBER: Exactly. Instead of 20 over 100. So, it's gone down. So, to protect your profit margin, you need to increase prices by more than the costs. So, this is kind of the first stage where this impulse translates into a larger price increase, simply to protect profit margins. Then what firms found is that this actually worked out better than they thought.

Volumes went down less than they anticipated, and they actually found that there is a lot of pricing space for them. And they kind of switched to a new type of playbook where they started to rely much more heavily on pricing than they used to. And that's not just one firm in isolation, but that is like many firms doing the same thing at the same time.

CHAKRABARTI: That's what we hear the Pepsi CEO ... saying, right? He said, rather than driving prices down, I don't think that's a big idea for anybody in the industry.

WEBER: Exactly. And you would hear statements like that not just from Pepsi, but from many, many firms across the whole spectrum of industries. So this is not just about consumer facing snacks. This is also about other types of food, like Nestlé, Unilever and so on. But also more upstream things like steel, like chemicals, like cars, which I mean, is consumer durable, different from snacks. So you would find these types of statements pretty much in a very far range of different types of companies.

CHAKRABARTI: Now, Professor Weber, before the break, you were talking about the shocks that everyone, individuals and companies felt as the pandemic hit, both due to the pandemic itself and the supply chain constraints together, and that led to an increase in prices. Makes a lot of sense. But you also then said that what companies found after some of those shocks ebbed a little bit was that consumer demand hadn't fallen or hadn't fallen dramatically. So what I wonder is, well, then, I mean, according to the most rudimentary rules of macroeconomics, if demand stays high, so should prices. So why isn't that an adequate explanation?

WEBER: Well, I mean, what we see is that on the company level, time and again, basically volumes start declining, but prices keep going up. So if it was simply about demand being strong, we wouldn't expect volumes to go down. Especially as the supply chain issues are easing, as the bottlenecks are easing. So if volumes are going down in a situation where the supply issues are becoming less dramatic, and prices still are going up quite by quite substantive amounts, then for these types of cases, and I'm emphasizing here cases, we are talking about a situation that I don't think can be explained by simply an increase in demand.

If it was simply about demand being strong, we wouldn't expect volumes to go down.

CHAKRABARTI: Okay. So we again, you've got this sort of tripartite theoretical argument that you say explains sellers' inflation, as you call it. We talked about the impulse stage, those initial shocks that causes companies to raise their prices. Now, we're in sort of the propagation and amplification stage that you have here as the prices continue to stay high. So let's return to our example of PepsiCo. A little earlier, we heard from a earnings call from the first quarter of 2021. Moving forward in time.

Here's a moment from their Q3 earnings call in 2022. So this is when executives spoke with analysts and investors in September of 2022. And it's interesting because they were asked. Pepsi executives were asked if they would consider price rollbacks, if there would be a general slowdown or a recession overall in the economy. And Ramon Laguarta, again, Pepsi CEO, responded to the question, saying the company did not have plans to reduce prices.

LAGUARTA: If you look at the majority of our conversation with our customers centered around growth and how do we develop our category, continue to bring consumers into the category, continue to bring new occasions into their category. And that's the role I think we played to our customers and to the how we create value for the company long term. So we'll continue with that focus, trying to create brands that can stand for a higher value to consumers. And consumers are willing to pay more for our brands. We'll continue with that philosophy.

CHAKRABARTI: So Professor Weber, you pointed out this moment in your paper about sellers' inflation, saying that there's no mention ... about rolling back prices if demand drops. But on the other hand, he's saying, well, we're just going to create higher value products that can sustain higher prices. So what's wrong with that?

WEBER: Well, I mean, this is one snippet from these kinds of earnings calls. There are also other moments where they talk about costs actually going down, but keeping prices where they are or even increasing them.

Now, if the input costs for stuff like energy, for basic raw materials and food are going down, then we would expect prices to also go down with them if profit margins were meant to kind of stay stable. But if prices stay where they are, then these declining costs actually mean another increase in in profit margins, potentially. This whole story around brands, I mean, there is a question of what is a brand, right? I mean, is this then really ultimately a different kind of product or is this a product where customers feel so attached to the idea of that type of goods as they.

I think this is from the Pepsi call. Saying at some point, we are selling a moment of pleasure, right? So they're really selling an emotion. They are selling a brand identity, which gives them a lot of pricing power, which gives them space to keep prices where they are or even increasing them, which I mean, you can interpret as an increased value for the customer. But at the substance, these kinds of products I think are still very similar to what they used to be. And it's really not like about the simple logic of demand going up and therefore prices going up or something like that.

CHAKRABARTI: So how long can this propagation or amplification stage of the sellers' inflation theory, how long can that go on for?

WEBER: I think that's a complicated question. I mean, what we are laying out in the ... framework to try to think about the dynamic of the current inflation rate. I think that ... all that we are seeing is pretty extraordinary. We are in very uncharted waters. So I think it's very hard to predict how long this can go on. My sense is that it's been going on for longer than I actually thought it could go on. How much longer it can go on is an open question and has to do with what happens in the conflict stage.

CHAKRABARTI: Okay. So, yes, how do you define what the conflict stage is?

WEBER: So we are thinking of the conflict stage as basically labor eventually reacting as prices are going up, as inflation is high and purchasing power is eroding. Eventually, workers may be asking for higher wages, right, to basically compensate the loss in real wages.

WEBER: Now, if wages go up, that of course, could create a new kind of impulse, because wages tend to go up in a sector kind of fashion because companies in one sector compete against each other and compete for a similar kind of labor pool. So if wages are going up in a whole sector, then this could be a similar kind of inputs as a specific input cost for one sector going up.

So it could be that firms then react to this by again increasing their prices in order to protect their profit margins, which could mean that inflation could go up again. But of course, there are so many variables at play that we cannot predict what will happen. But I think this is one possibility, one possible avenue that we can see from where we stand.

We are in very uncharted waters. So I think it's very hard to predict how long this can go on.

CHAKRABARTI: Well, what's interesting, though, is that the presumption is that wages would go up meaningfully. And as I quoted earlier, former Fed vice chair Lael Brainard earlier this year talked about that the labor share of income has declined over the past two years in comparison to, I guess, the profit or capital share. So that's an interesting note, even though I guess the exact dollar value of wages has gone up. But again, just to stick with Pepsi as our sort of real-world example here, and yes, these are just, you know, individual moments from 45-minute-long earnings calls, but they're indicative here.

So I've got one more that might talk us through a little bit about how some companies are at least looking or eyeing at what you're calling the conflict stage here. So this is from Pepsi's 2022 Q4 earnings call. So it just happened a few months ago in February of 2023.

And interestingly, analysts, the first question in the earnings call, the very first question came from an analyst who asked executives if they were worried about consumer and retailer pushback about Pepsi's continued historically high prices and whether or not the company was planning for what the analyst called incremental consumer weakness. So here's how Ramon Laguarta, Pepsi CEO answered. He said there could be some changes in consumer behavior in the second half of the year, but the company was still aiming for a 6% top line growth.

LAGUARTA: We feel comfortable with the way the business is going, as you could saw from Q4. But, you know, the key, the most important thing for you to think about is we're going to keep investing in the quality of our products. We want to keep investing in the strength of our brands. So no matter what happens with the consumer, we're going to be, I think, preferred choice for a lot of our consumers and, you know, our customers. And that's how we are planning for next year.

CHAKRABARTI: Professor Weber, how do you what do you hear in that?

WEBER: Yeah, I think this point of being the preferred product of the customers is an important one here, where basically a company like Pepsi has such a strong market position that they can meet demand wherever it is, as they are saying, whether it's in a pandemic and restaurants are shut down and consumers go to supermarkets, they will end up still buying Pepsi.

If they now go to the restroom, they buy Pepsi. If their income declines and they end up no longer going to the restaurant, but just maybe stopping at a gas station on the way to work, they would still buy a Pepsi. So in other words, the consumer is bound so strongly to this brand that they seem to be very confident in being able to keep consumers with them, even though they have been pursuing this strategy of increasing prices and prices over volume for quite some time by now.

CHAKRABARTI: So before we get into some of the still quite vigorous pushback to your theoretical framework of sellers' inflation or greedflation, as we in the media have taken to calling it. I do want to note that, again, we're having this conversation because there's a lot of people in very high levels of businesses and organizations in the global economy who are suddenly talking about this.

Because as you know, Professor Weber, just a couple of months ago in March, Paul Donovan, who's the chief economist at UBS Global Wealth Management, he wrote a note also talking about what he described as profit margin led inflation. And stating that most of the time in typical economies, companies have weak pricing power because there's just a lot of response from consumers in moderating their demand.

And they just can't wildly increase prices, because consumers will abandon them. But that hasn't happened this time around. So there's a lot of people paying attention to you at the moment. Nevertheless, there's also a lot of pushback. So I want to explore some of that. First and foremost, Professor Weber, especially in the United States, what about the simple macroeconomic fact that the government pumped a whole lot of money into the economy as pandemic aid, as a means to prop up the economy, to help people through unemployment. And there's just a lot of cash looking for a constrained amount of goods because of the supply chain crisis we have. That's just kind of the basic scenario for inflation. How does that not explain everything we're seeing?

WEBER: Well, I think the critical point that you are bringing in here is the supply chain story. Right? And what we have seen is that bottlenecks have presented opportunities for firms to increase prices. So if you imagine a firm being confronted with a bottleneck like, for example, a chip shortage, and they know that their competitor also is facing a similar kind of shortage.

This means that when they increase prices, they are no longer worrying that customers would run away from them, because their competitor is in the same kind of situation and is very likely to react with the same kind of price increase. So in other words, we have been living in an incredibly concentrated kind of economy before the pandemic. But during the pandemic, with these supply shocks, we have entered a world where price hikes could be coordinated by these emergencies, by these bottlenecks, by consumers also being more willing to pay these higher prices, because it seems legitimate to them that these prices are increasing.

Because they are seeing on the news that supply chains are crumbling, because they are seeing on the news that energy prices are going up and so on. So I would think of a demand here as an enabling factor, but I don't think it's the key factor. Because if demand was going up, and firms were worried about losing their customers, if they were increasing prices because other firms were not increasing their prices, then I don't think they would be doing it. So the key factor here really is that the dynamic of competition has changed.

What we have seen is that bottlenecks have presented opportunities for firms to increase prices.

CHAKRABARTI: So I mean, to me, that leads us down the road a little bit later about talking about how in some of these sectors there's a problem of inadequate competition. Right? We have virtual monopolies in some of these sectors, but we'll come back to that in a second. I did want to offer you sort of a counterargument that comes from Justin Wolfers.

He's a professor of public policy and economics at the University of Michigan. And he says, basically, with all due respect, the evidence points to a different conclusion that profit seeking isn't a driver in hidden inflation. We're seeing it all, according to Wolfers. And he told us that recent numbers from 2022 discount your idea of sellers' inflation.

WOLFERS: The claim that low unemployment has sparked inflation has a lot of historical evidence, global evidence. The claim that the supply shocks associated with either Putin or the pandemic has enormous global influence evidence because we saw the same thing happening in almost every country around the world.

The claim that this is in the set of theories that are sometimes called greedflation, doesn't have a lot of independent evidence in favor of it. A simple thing to note is since the middle of 2022, corporate profits have fallen by 7% or 8% and prices have risen by 5% or 6%. That seems a rather embarrassing fact for those claiming that greed and the pursuit of higher profits is what's causing higher prices.

CHAKRABARTI: Professor Weber, your response?

WEBER: I mean, first of all, let me be crystal clear. If you read my paper, you will see that I'm not blaming the increase of inflation on a sudden jump in corporate greed. I'm also not using the term greedflation, because I think what we are seeing is not a sudden change in the attitude of firm leaders. But what I'm arguing is that the dynamic of competition has changed. When firms were faced with bottlenecks, when these major cost shocks, coordinated price hikes. So in that sense, I'm fully with my colleague and saying that these major supply shocks have been very, very important.

... What we are arguing is that firms don't absorb these cost shocks, but rather they pass them on. And in certain consultations they can even amplify these kind of cost shocks. To the question of some ... profit margins going down in 2022. First of all, there has been reporting by Bloomberg that there are some questions whether the Federal Reserve is included in this data, but this is not my main point. My main point is that in 2021, profit margins have chomped up in a very dramatic fashion reaching levels that we hadn't seen since the aftermath of World War II.

Them easing somewhat in 2022 is entirely consistent with our theory, because we don't argue that this may be inevitably a sustained process of constantly elevated profit margins. But we say that there's an impulse that presents an opportunity for firms to hike prices, for some firms to hike prices more than costs, thereby driving up profit margins, but that this eventually goes into the conflict stage where we would expect profit margins to come down. So this is absolutely consistent with my theory.

CHAKRABARTI: I did read your entire paper and I found it to be utterly fascinating, particularly the fact that you and your coauthor went through in detail to look at what executives were saying in earnings calls. And did you do that because, you know, it's one of the windows into the just the sheer decision-making apparatus beyond what the bottom line might say in corporate documents. This tells us how and why executives are making the decisions they are.

WEBER: Yeah. I mean, we are in a situation where a lot of things are happening at the same time. It's a pretty unprecedented situation of overlapping emergencies with the war and with the pandemic. And to understand how firms are reacting to this, I think we cannot just assume, oh, it's supply demand and then draw a little diagram with two linear curves.

But it's helpful to look at what the corporate leaders are actually saying about price setting, how they're actually thinking about pricing and how they themselves portray the role of pricing in their firms' strategies. So in a way, there is this treasure trove of data sitting out there that we can dig into that is publicly available. And that, I think, gives us a whole new perspective on the dynamic of price increases.

It's a pretty unprecedented situation of overlapping emergencies with the war and with the pandemic.

CHAKRABARTI: So we listened a little bit to several earnings calls from Pepsi. That was one example. But overall, how would you summarize what you heard and read in the transcripts of the earnings calls that you looked at from, you know, everyone from Pepsi to Procter and Gamble and others?

WEBER: Well, I would say that costs do play an important role. That's why we are emphasizing that there's an initial impact stage. And that firms initially react to these kind of cost shocks. And I would say that one of the primary goals of corporate leaders is to protect their profit margins. I would also say that on these earnings calls, when analysts from, for example, Morgan Stanley, just to give one random example, are asking about pricing, they are of course not asking as an uninvolved academic just seeking some information, but they are asking as a representative of a very major bank that potentially would be holding shares in these firms.

So we also have a certain dynamic there of shareholders possibly exercising a certain degree of pressure on companies to pursue exactly that kind of strategy, because that's what they are seeing in other companies. I would also say that we see in these earnings calls that often corporate leaders express a certain degree of surprise. Just how building customers were to sustain these higher prices so that in some sense they also discovered just how much pricing power they have in this process.

CHAKRABARTI: But isn't that one of the unusual things about this moment, because that flies in the face of, again, sort of basic macroeconomic theory.

WEBER: Yeah. I mean, Tracy Alloway at Bloomberg has coined this whole phenomenon on the consumer side as 'excuseflation,' which I think is a good term, capturing that customers do behave differently in a global emergency. Where if you imagine you go to a store every day and then suddenly prices go up and you don't have a very good reason why prices went up, you probably would find it illegitimate and you would try to switch to another store.

But if you are hearing on the news all this information on the emergencies that, of course, impact the economy, then this also changes something in the attitude of consumers, which seems to make them more willing to pay these higher prices. Of course, in some areas we are also talking about necessities.

So when, for example, Procter and Gamble is explaining that they are selling all types of diapers, the most luxurious and the simplest type, and that if prices go up, parents might switch from the luxuries to the less luxurious brand, but they would still buy from Procter and Gamble. Then this also shows us that there are areas of essentials where consumers simply don't have a way to reduce demand in ways that would make them go away from certain kind of firms that really are occupying very dominant positions in the market.

CHAKRABARTI: That's the competitive landscape has changed part, right?

WEBER: I mean, I'm not even sure if it has changed, to be honest, because we already had incredibly concentrated markets before the pandemic. But in the situation of emergency, faced with these cost shocks, faced with this different mindset on the part of the consumer, and corporations could use their position in the market in a new kind of way.

CHAKRABARTI: Okay. So to that point, I just want to play again a little bit from Justin Wolfers at the University of Michigan, who just disagrees with your framework. ... And he says, of course, while it's objectively true that firms have been raising prices, even though you're looking to the how's and the why's in earnings calls, for example, Justin Wolfers says he doesn't actually see that there's a clear reason why corporations have been continuously raising their prices.

WOLFERS: Is it because they're greedy? Is it because they can? Is it because they can in 2023, But they couldn't through the rest of American history. Is it because their costs are rising? Well, we can observe their costs. But maybe is it because their future costs are rising? We can't observe their future costs. Is it because they think consumers are flush with cash right now? Is it because they expect to sell out if they don't raise their prices? It could be any of these.

I'm not confident that I know which of those that it is, but I would rely on the historical record to help me figure out what are the main drivers of inflation. I would rely on economic theory, and I would simply ask the question, what is it that is so different about 2021 through 2023 that means we now blame profiteering. But such profiteering wasn't possible in 2019, when we had fairly similar levels of corporate concentration. A fairly equally hot economy and perhaps not as many changes in the cost structure. So there are some differences and there are some similarities.

CHAKRABARTI: So, Professor, I think you've already given your answer to that. What is different? The difference is the pandemic. The difference was the emergency.

WEBER: Yeah. I mean, first of all, I agree with the question that he's posing here. In fact, that is the question that we are raising in our paper. And I think this requires us to look back to how we see pricing before the pandemic. And I would argue that in these highly concentrated sectors where firms are price makers, there is a logic of not under bidding prices because you don't want to start a price war because that could reside into a destructive kind of competition where if only a few number of companies have very high stakes in one market, they don't want to destroy that market.

But at the same time, they don't want to increase prices when they cannot be sure that their competitors are following suit, because if they did, they would lose market shares and they would basically harm themselves. And in an age of globalized production, in an age of incredibly powerful global production networks, something that we haven't seen in human history, I mean, the efficiency of these supply chains is just mind boggling, right?

This also means that if one company increases their prices, the competitor can very easily accommodate that demand. Why are these supply chains up and running and working like a smooth and global clockwork so that the pressure of competition is really very high? But once there's sand in this clockwork of global production, once it's no longer clear that your competitor could meet that demand, once there is a cost shock that hits a whole sector, and that actually sends a very clear signal to all firms in this market that this is the time to raise prices.

Once there is a cost shock that hits a whole sector ... that actually sends a very clear signal to all firms in this market that this is the time to raise prices.

Once they raise prices and they find that their customers are not running away in sufficiently large numbers to bring down their profits, but that they can actually increase their profits, they keep doing that as everybody else is doing it. And you kind of have entered a new type of game.

CHAKRABARTI: Okay, New type of game. I just, I have to ask how it feels to get the kind of response and pushback that you did both in 2021 and, and even now. People just saying, your theory is nuts. ... I'm thinking back to when a former Fed chair in in the United States called economics the dismal science. I feel like the world of economists is one that's kind of crotchety and doesn't necessarily like radical theories that rock the boat a little bit. I mean, is that part of what's going on here?

WEBER: Oh, yeah, for sure. But the world of economics is also one that we see based on pretty good empirical evidence as one that is incredibly sexist, as one that is incredibly penalizing to anyone who is holding different kinds of views and so on. So it's certainly one that is not very open to new perspectives, which I think is really a problem. If we are in a situation that I think is incredibly complex, that in many ways is very new.

I mean, we haven't lived through a global pandemic in 100 years. We haven't had war in Europe. I mean, thank God we didn't have war in Europe in a pretty long time. We haven't lived through climate change. We haven't experienced the frequency of extreme weather events that we are experiencing. We have probably never been in a situation where all of these things are happening at once and we have incredibly concentrated kinds of corporate sectors.

So I think we are in a pretty new constellation in a pretty intense situation of emergency where I think we really need an open discussion where everybody's contribution is, from the onset, taken as a serious and genuine contribution, trying to understand what's going on instead of some sort of a conspiracy theory, instead of some sort of attack against the perceived wisdom or whatever. Yes, I think we really need a new kind of a culture of debate to be part of the solution of the enormous challenges that our societies and economies are facing today.

CHAKRABARTI: And by the way, your use of that phrase, conspiracy theory, that's what your sellers' inflation framework was called by some people. I saw Catherine Rampell in The Washington Post said that there's a conspiracy, an economic conspiracy theory infecting the minds of certain lawmakers in Washington. But quickly, Professor Weber, you mentioned economics being quite sexist. Do you think that's part of what's at play here, that you know, oh, there's that woman over in Amherst, Massachusetts, talking about erratic or excessive profit seeking as a driver of inflation.

WEBER: I mean, I certainly don't think it can be reduced to that, but I think it's part of the story. Being a young woman, if you say something new and different, the presumption is often that you just didn't get the basics and you just don't understand how Econ 101 works. And in fact, that is not just me making that claim, but that is what people literally wrote on Twitter, right? Like saying, oh, how can she have a pitch in economics? She clearly must have failed Econ 101.

Whereas if someone in a different kind of position with a different identity might make similar points, they might be perceived in a different kind of way. But again, I don't think it can be reduced to this. I think it really also is a situation in economics where we need a more open discussion in the sense of an openness for a pluralistic approach to economics.

CHAKRABARTI: Well, I wouldn't reduce it to sexism. Agreed. Just like your approach to viewing inflation now is not exclusively reduce to sellers' inflation. You're saying it's a part of this overall complex, sort of uncharted territory that we're in at the moment. Point taken on that. It just occurred to me, though, that in the past, the world of economics has eventually come around to embracing what was once considered pretty radical theories.

Like the idea of shareholder primacy being a huge driver in corporate decision making wasn't necessarily always the case, but it became economic orthodoxy in the United States, at least, you know, in the 60s and 70s. So now we've just got a couple of minutes left. Professor Weber, with this framework in mind, sellers' Inflation as a contributing factor to the unusual kind of inflation we're seeing in this crisis, in this emergency, of course, the question is what to do the next time around. That is where you really rankled a lot of people, when you suggested perhaps price controls. Now you just got about 2 minutes left here. The word price control sort of generates all sorts of economic nightmares, right, about causing the collapse of economies, essentially. So what do you mean by price controls and how would that work in the next crisis?

WEBER: So I think what we really need is a form of economic disaster preparedness so that we would contain these cost shocks at the impart stage before they rippled through the whole economy and create a lot of disturbance in their wake. Ideally, we would mobilize things like the Strategic Petroleum Reserve, which by the way, the U.S. did in 2022.

What we really need is a form of economic disaster preparedness.

... But if you do not have a strategic petroleum reserve, if you have no disaster preparedness and then you have this gigantic kind of shock, price controls can buy some time in order to achieve a correction of the shortfall of supply. Of course, they're not going to correct the shortfall of supply by themselves, but this time bought can be important if it then prevents these kinds of knock-on effects. And we have seen that in Europe. We now have a European gas price cap which contributed to calming the markets on gas because there was no longer an expectation that gas prices could just climb in an unlimited kind of fashion. And that kind of expectation, that kind of signal to market participants is also really important.

This program aired on June 2, 2023.